Introduction

This report presents the findings of a study conducted by Eurekahedge analysts on more than 1,000 SRI funds. The aim of this research report is to find the aspects of the industry in 2010, such as where the funds are investing, which sectors and asset classes and what are the different criteria being employed.

Socially responsible investment schemes, SRIs for short, are funds that seek to incorporate a variety of moral and ethical principles into their investment decisions. As such, in addition to traditional quantitative assessment of risk/return profiles, asset managers also employ increasingly sophisticated environmental, social and governance (ESG) criteria to screen for potential investments. Also known as ethical or socially conscious investing, the concept is not new and has been around since the 19th century; however, recent world events and increasing reach of information and spread of ideas have garnered greater attention for this sector.

While the origins of social investing lie in negative screening based on religious concepts, the categories within SRI’s have expanded rapidly over the last 50 years to encompass various ideological and political sentiments. Currently, the most widespread criteria employed by SRI funds include environmental record, human rights and corporate governance. For a more detailed discussion on the history, evolution and concepts of socially responsible investments in different parts of the world, please refer to the various articles[1] on the Eurekahedge website.

Changes in the Number of Funds and Assets under Management

Figure 1 shows percentage changes in the number of funds and industry assets over the last three years.

Figure 1: Percentage Growth in SRI Funds

Through the 2008-2009 period, SRI funds suffered significant losses due to the movements in the markets. The decrease in assets was proportional to the decline in global equity markets, which make up the bulk of SRI investments. Furthermore, by the end of 2009, the number of funds operating also shrunk by 6%, although overall industry assets increased during the year. The first six months of 2010 have seen some losses in assets under management; however, the rate of closures has fallen and going forward, we expect the trend of attrition to reverse by the end of the year.

Performance Review

Figures 2a-2b: Eurekahedge SRI Fund Index vs MSCI World Index and Dow Jones World Sustainability Index

While the performance of SRI funds tends to closely follow that of global equity indices, we have seen SRI funds outperform the markets over the last 12 months and also in the long term, albeit marginally. Furthermore, the 2008 returns and the June YTD returns of SRI funds show significant downturn protection offered by the funds when compared with equity markets. At the same time, SRI funds were not able to capture the heavy upsides in the years preceding the financial crisis. These performance trends are in accordance with the stricter risk management practices of SRI funds.

Table 1: Eurekahedge SRI Fund Index vs Various Indices

Long Only Absolute Return Funds

|

SRI Funds

|

MSCI World Index

|

Islamic Funds

|

DJ World Sustainability Index

| |

2009 Returns

|

46.93%

|

22.89%

|

22.82%

|

21.52%

|

36.06%

|

Jun 2010 YTD Returns

|

-0.77%

|

-3.41%

|

-8.14%

|

-1.16%

|

-12.93%

|

3-Year

Annualised Returns Jun-07 – Jun-10

|

-4.78%

|

-7.11%

|

-13.41%

|

-2.19%

|

-11.92%

|

3-Year

Annualised Volatility Jun-07 – Jun-10

|

20.64%

|

14.92%

|

20.00%

|

12.66%

|

24.25%

|

Figure 3: SRI Funds Performance by Asset Class

Asset Class

Figure 4: SRI Funds by Asset Class and Industry Focus

While most SRI funds invest in equities, an increasing number of managers have started using other products. On the other hand, the industry-wise breakdown of the SRI space is well-diversified in terms of sectors. The next table gives the lists of the different industries and the criteria employed in positive and negative screening by the funds.

Definition

|

Positive/Negative Screen

| |

Aerospace/Defence/Weapons

|

Avoid investing in companies involved in the production/marketing of weapons.

|

Negative

|

Animal Testing/

Animal- related

|

Investor sentiment in favour of humane treatment of animals. As such, firms practicing product testing on animals, as well as those that manufacturing hunting equipment, are avoided. Investments in companies that support welfare of animals are encouraged by positive screening funds.

|

Positive and/or Negative Screen

|

Tobacco/Alcohol-related

|

Investments in tobacco and alcoholic beverage businesses are avoided.

|

Negative

|

Gambling-related

|

Investments in casinos and gambling equipment suppliers are avoided.

|

Negative

|

Pornography/Child Labour

|

Investments in the porn industry are avoided. Firms that employ child labour anywhere in the supply chain are also avoided.

|

Negative

|

Environment

|

Seek and support firms with proactive involvement in ecologically friendly business activities. Shun firms with reckless environmental track record and large carbon foot print.

|

Positive and/or Negative Screen

|

Human Rights

|

Seek and support firms with a good human rights track record while avoiding those with poor records.

|

Positive and/or Negative Screen

|

Employee Benefits/Labour

|

Funds invest in those firms that meet high standards of positive labour policies while those firms with a track record of exploitation are avoided.

|

Positive and/or Negative Screen

|

Customer/Product Advocacy

|

Seek firms acting in the best interest of the consumers and using ethical advertising in their product marketing. Avoid firms making spurious claims and products.

|

Positive and/or Negative Screen

|

Nuclear Power

|

Seek firms using nuclear power to reduce our dependence upon oil/coal powered energy. Shun firms involved in the production and operation of nuclear reactors used solely for the intent of producing weapons of mass destruction.

|

Positive and/or Negative Screen

|

Alternative Energy /

Biotechnology

|

Seek and support firms with a proactive approach to harnessing environmentally friendly and renewable sources of energy.

|

Positive

|

Corporate Governance

|

Invest in firms that maintain high standards of responsibility and transparency in CSR issues. Avoid firms with a record of scandals and fraudulent activities.

|

Positive and/or Negative Screen

|

Company Investments / Foreign Operations

|

Seek companies committed to research and development, both home and abroad with considerable positive social benefits. Shun firms investing in technology or infrastructure that harms the environment or has considerable negative social costs associated with it. Firms with operations in countries with oppressive regimes are also avoided.

|

Positive and/or Negative Screen

|

Community/Social Issues

|

Invest in firms that are involved in community building projects by sponsoring employee volunteering projects and other such programs.

|

Positive

|

Positive and Negative Screening

Socially responsible funds employ positive and negative screens as the primary method to identify the companies that they wish to invest in or wish to avoid investing in. Figure 5 gives the breakdown of screens used by SRI funds.

Figure 5: SRI Funds Screens Employed

Positive Screens

As implied by the name, positive screening funds utilise research methodologies to identify the companies that they are interested in investing. For example, a fund which has environmentally conscious investors will look for companies that have a good environmental track record and will also be interested in allocating to green technology and clean energy firms. Most of the funds that employ positive screens have more than one criterion. Figure 6 shows the breakdown of screening criteria used by SRI funds (eg nearly 80% of all positive screening funds look at the environmental record of firms before deciding to invest).

Figure 6: Criteria Distribution of Positive Screens Employed

Negative Screens

Negative screening funds avoid investing in those firms that are involved in activities deemed to have a negative social impact. For example, firms that are involved in the manufacturing and marketing of weapons are avoided since their products are utilised in times of war.

Figure 7: Criteria Distribution of Negative Screens Employed

Both Positive and Negative Screens

Some funds employ both negative and positive screens in their investment decisions. For example, while some funds will avoid firms which have a bad environmental record (negative screen), others will actively seek those firms which have an excellent environmental record or are involved in the environmental sector and the development of green technologies (positive screen).

Figure 8: Criteria Distribution – Positive and Negative Screening SRI Funds

Geographies

While most SRI funds are located in Europe and North America, nearly 50% follow a global-investing mandate while some funds are focused on Asia and developing markets. There are also some funds focussing specifically on African and Africa-investing firms.

Figure 9: Assets across Geographies

Manager Location

The SRI world can be split into European funds, which form 58% of the universe, and non-European funds. The charts that follow look at the differences between European SRIs and those from the rest of the world (RoW).

Figures 10a-10b: Fund Manager Locations by Number of Funds

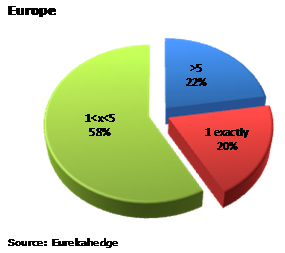

Figure 11: Number of Criteria employed by SRI Funds

Among different SRI funds, there are those which are focused on particular issues, such as environmental issues only. However, the recent trend has been to add an increasing number of criteria to the screen potential investments. Figure 11 gives the breakdown of the number of criteria used by European managers and non-European managers while Figures 12 and 13 show what percentage of funds screen for particular criteria.

Figure 12: Criteria Breakdown - Europe

Figure 13: Criteria Breakdown – Rest of the World

Conclusion

Socially responsible investing is becoming more and more prevalent as the global focus on themes such as climate change and human rights increases. Investor sentiment has, over the years, changed from “maximising profits” to “maximising profits while investing in an ethical manner”. In addition to the swing in public opinion, other important contributing factors include legislative and government pressure, such as US President Obama’s support for the global fight against climate change, EU legislations on CSR and the latest EU Conference on Corporate Social Responsibility held in March 2010.

Furthermore, the criteria being employed for socially responsible investing are also increasing along with new schemes of investments, such as the microfinance in third world countries. While at this point, there is no industrywide set of rules and regulations for socially responsible investing (such as the compliance to Shariah board in Islamic funds), some funds have already started to adopt the UN Principles for Responsible Investments as a benchmark and going forward, this may become the standard practice as the industry matures.

While the performance of socially responsible funds has not matched that of absolute return vehicles such as hedge funds, it must be noted that they have outperformed the underlying markets over the last three years with less volatility in returns. Additionally, the increasing focus on CSR, which includes issues of transparency, effectively decreases the possibility of fraudulent activities being conducted by firms and hence, also serves as a tool for better risk management.

Going forward, we expect the SRI funds industry to continue attracting capital, with the number of funds continuing to increase. Also, we expect an increasing number of existing funds to adopt some sort of screening criteria in accordance with the rising demand from investors and legislatures.

Superb!! I have already bookmarked your blogTrikle Trade

ReplyDelete