Introduction

Asian hedge funds have witnessed remarkable growth over the last decade in terms of both fund population as well as assets under management (AuM). As at August 2011 the total AuM in Asian hedge funds stood at US$135 billion; nearly six times that as of end-2000 while the number of funds increased more than six fold in that same period.

Although assets managed by Asian hedge funds peaked in 2007 at US$176 billion, the size of the region’s hedge fund industry was hit by the combined effect of redemptions and performance-based losses through the global financial crisis causing AuM to fall to US$105 billion in April 2009.

Figure 1: Industry growth since 1999

Since April 2009 the industry has witnessed healthy growth, gaining nearly US$31 billion over a period of 28 months. During this time the Eurekahedge Asian Hedge Fund Index has gained 27.4% leading to performance- based gains of more than US$15 billion. Record performance in 2009 also encouraged investors to allocate capital to the regional hedge funds. Over the last 12 months the sector has attracted nearly US$11 billion through net positive asset flows.

|

|

Asset flows

Table 1 details the monthly changes in AuM from January 2009 to 2011 YTD. In the first half of 2009, Asian hedge funds continued to witness heavy redemptions from investors, losing a total of US$26 billion. As managers started to post healthy gains on the back to rallying underlying markets, investor sentiment improved and the sector witnessed some net positive asset flows in 2H 2009.

Asian hedge funds started 2010 with expectations of strong inflows based on excellent 2009 returns and healthy allocation activity seen at the end of 2009. However after an initial period of profit-taking and portfolio rebalancing, a norm at the start of the year, most investors withheld allocations until the second quarter of the year amid concerns over European debt contagion spreading to emerging markets and Asia. Investor sentiment improved from May 2010 and since then the sector has gained US$12.8 billion through net positive asset flows.

Table 1: Monthly asset flows in Asian hedge funds

Month

|

Net Growth (Performance)

|

Net Flows

|

Assets at end

|

Jan-09

|

0.1

|

(9.1)

|

117.4

|

Feb-09

|

(0.2)

|

(4.7)

|

112.5

|

Mar-09

|

0.6

|

(4.6)

|

108.5

|

Apr-09

|

1.3

|

(5.1)

|

104.8

|

May-09

|

3.6

|

(2.6)

|

105.8

|

Jun-09

|

0.4

|

(0.2)

|

106.0

|

Jul-09

|

1.6

|

0.5

|

108.1

|

Aug-09

|

(0.2)

|

1.7

|

109.6

|

Sep-09

|

1.0

|

1.2

|

111.9

|

Oct-09

|

(0.0)

|

2.8

|

114.6

|

Nov-09

|

0.9

|

1.0

|

116.5

|

Dec-09

|

0.9

|

(0.1)

|

117.3

|

2009

|

10.1

|

(19.1)

|

117.3

|

Jan-10

|

(1.2)

|

(0.6)

|

115.6

|

Feb-10

|

(0.2)

|

(0.7)

|

114.7

|

Mar-10

|

2.2

|

(0.1)

|

116.8

|

Apr-10

|

0.9

|

(0.4)

|

117.3

|

May-10

|

(2.4)

|

0.7

|

115.5

|

Jun-10

|

(0.3)

|

0.4

|

115.6

|

Jul-10

|

1.1

|

0.5

|

117.1

|

Aug-10

|

0.4

|

0.4

|

117.9

|

Sep-10

|

2.8

|

0.5

|

121.1

|

Oct-10

|

1.8

|

1.9

|

124.8

|

Nov-10

|

0.2

|

0.7

|

125.7

|

Dec-10

|

2.0

|

0.8

|

128.6

|

2010

|

7.2

|

4.0

|

128.6

|

Jan-11

|

(0.5)

|

0.3

|

128.3

|

Feb-11

|

(0.1)

|

1.6

|

129.8

|

Mar-11

|

0.8

|

0.3

|

130.8

|

Apr-11

|

1.7

|

1.1

|

133.6

|

May-11

|

(1.2)

|

2.1

|

134.5

|

Jun-11

|

(0.9)

|

0.7

|

134.3

|

Jul-11

|

1.3

|

0.5

|

136.1

|

Aug-11

|

(1.2)

|

0.4

|

135.3

|

Note: all figures are in US$ billion Source: Eurekahedge

Launches and closures

After witnessing a high attrition rate in the 2H 2008 to 1H 2009, the population of Asian hedge funds has reverted back to a healthy growth trend. A total of 351 new funds have been launched since July 2009, as opposed to 236 fund closures. While launch activity has been encouraged by healthy performance of Asian hedge funds and strong growth in the underlying markets, attrition rate has fallen due to reduced redemption pressure as well as an increasing number of managers having been able to meet their high watermarks, and hence generate performance fees.

Figure 2: Launches and closures across Asian hedge funds

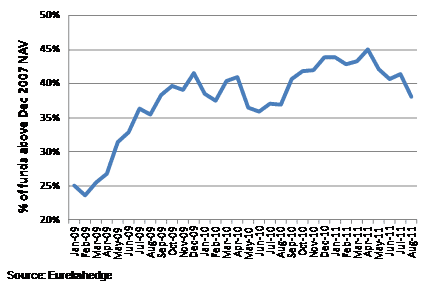

High watermark

As the high watermark differs from investor to investor depending on the net asset value (NAV) level at the time of capital allocation, we take the NAV of funds at December 2007 as the starting point for this analysis to determine if they are above their high watermarks.

Figure 3: Percentage of managers above 2007 December NAV

Fund Size

The current distribution of fund population according to AuM shows a significant difference from four years prior due to the strong directional trends in performance, heavy redemptions and high attrition rate suffered by the industry through the financial crisis. The percentage of funds managing US$50 million or less has increased from 54% in 2007 to 64% in 2011, suggesting that new launches have not attracted much capital and most of the allocations witnessed since 2H 2009 have gone to larger funds.

Figures 4a-4b: Breakdown of fund population by fund size

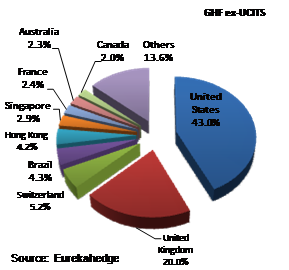

Geographic mandates

In terms of geographic investment mandates, the assets invested in globally mandated funds have witnessed the greatest growth. As globally investing funds did not suffer losses of the same extent as other Asian hedge funds in 2008, most of the capital allocated to hedge funds over the last two years came from institutional investors who prefer to invest in large global-mandated funds to gain exposure to Asia. The drop in the share of Asia including Japan and Japan focused funds, is primarily due to the closure of a few large funds over the last four years as well as the greater relative growth of global and China investing funds.

Figures 5a-5b: Geographic mandates by AuM

Strategic mandates

The most important trend here has been the decline in the share of long/short equity funds. The Asian hedge fund space was initially dominated by long/short equity hedge funds as it was the easiest implemented strategy that investors have traditionally been most comfortable with. However, easing of restriction in markets such as China and India, greater access to the markets and the growing availability of more complex financial instruments in Asian markets, has led to an increasing number of funds that employ different strategies. Additionally, long/short equity funds lost a major chunk of assets through the financial crisis due the rapid decline in equity markets globally.

Figures 6a-6b: Strategic mandates by AuM

Head office locations

The distribution of Asian hedge funds population by head office location also shows some significant trends that point to a maturing industry. In 2007, 40% of the funds were managed out of the UK and the US, as these were the traditional hedge fund centres. Over the last four years however, Hong Kong and Singapore have gained substantial market share from New York and London. The continued expansion of service providers in Asia, proximity to region of investment, and an increasingly large financially trained workforce have helped this move towards Asian-based funds.

Figures 7a-7b: Head office locations by number of funds

Prime brokers

Tables 2a and 2b display the breakdown of Asian hedge funds assets according to their 2007 and 2011 prime brokers. The trend shows more equitable distribution of assets across the top 10 prime brokers as managers have started to use more than one prime broker as a measure to manage counterparty risk. The decreasing share of ‘Others’ also shows that funds prefer to work with larger, renowned and financially stable prime brokers in the post-Lehman world. New prime brokerages in the region have found it hard to break into the hedge fund business, and as such they have targeted niche sectors and the smaller hedge funds to gain a foothold in the sector.

Tables 2a-2b: Top prime brokers by market share

2007

|

Prime Broker

|

Market Share

|

Goldman Sachs

|

26.49%

|

Morgan Stanley

|

26.62%

|

UBS

|

9.15%

|

Deutsche Bank

|

7.50%

|

Credit Suisse

|

6.60%

|

Citigroup

|

3.23%

|

Merrill Lynch

|

3.77%

|

Bear Stearns

|

9.13%

|

Fimat

|

0.53%

|

Others

|

6.98%

|

|

August 2011

|

Prime Broker

|

Market Share

|

Goldman Sachs

|

28.41%

|

Morgan Stanley

|

24.38%

|

UBS

|

13.24%

|

Deutsche Bank

|

8.87%

|

Citibank

|

8.30%

|

Credit Suisse

|

4.56%

|

Bank of America Merrill Lynch

|

4.40%

|

Newedge

|

2.35%

|

Barclays

|

2.10%

|

Others

|

3.38%

|

|

Source: Eurekahedge Source: Eurekahedge

Administrators

The trend towards more diversification within the larger service providers is also apparent in the breakdown of hedge fund assets by administrators. HSBC continues to take the top spot as the largest Asian hedge fund administrator by market share - however the percentage share has fallen from 32.17% to 19.12% over the last four years. State Street has increased its share significantly with increased focus on Asia as well as the acquisition of Mourant International Finance Administration. The most noteworthy trend is the near 10% drop in the share of assets administered by ‘Others’, which includes in-house administration. The primary reason for this shift is the emphasis on regulations and transparency as no investor is willing to invest with managers lacking proper risk controls in place and reputed third-party administrators.

Tables 3a-3b: Top administrators by market share

2007

|

Administrator

|

Market Share

|

HSBC

|

32.17%

|

CITCO

|

10.76%

|

State Street

|

4.94%

|

Citigroup

|

4.11%

|

Goldman Sachs

|

3.36%

|

PNC

|

2.91%

|

JP Morgan

|

2.40%

|

Morgan Stanley

|

2.03%

|

Fortis

|

1.98%

|

Northern Trust

|

1.95%

|

Others

|

33.38%

|

|

August 2011

|

Administrator

|

Market Share

|

HSBC

|

19.12%

|

CITCO

|

11.97%

|

State Street

|

11.89%

|

RBC Dexia Investor Services

|

9.81%

|

Morgan Stanley

|

7.19%

|

GlobeOp

|

4.32%

|

Citibank

|

3.57%

|

Goldman Sachs

|

2.93%

|

JP Morgan

|

2.70%

|

Meridian Fund Services

|

2.47%

|

Others

|

24.01%

|

|

Source: Eurekahedge Source: Eurekahedge

Performance review

The performance of Asian hedge funds against the underlying markets and other alternative investments is seen in figure 8. Asian hedge fund managers outperformed Asian funds of funds and Asian long-only absolute return funds over the last five years. During the financial crisis in 2008 to 2009, the long-only index shed the most percentage points with a 51.15% drop from peak to trough while Asian hedge funds lost a maximum of 30.98%, displaying better downturn protection. Asian long-only funds also have a high beta with underlying markets as opposed to Asian hedge funds. When compared against the MSCI AC Asia Pacific Index, long-only funds registered a beta of 0.86 while hedge funds had a beta of 0.41 over the last five years.

Figure 8: Performance of Asian hedge funds vs. other investments since 2006

Within Asia, hedge funds allocating to Greater China have been the most profitable over the last three years with returns of 38.92%. In comparison, the Shanghai Composite Index only gained 9.21% in the same period of time. Funds investing in developed markets in the region; Australia/New Zealand and Northeast Asia have delivered more consistent performance recently.

Figure 9: Performance of Asian hedge funds across geographic mandates

Table 4: Performance of Asian hedge funds across geographic mandates

|

Asia

|

Asia

ex-Japan

|

Australia/

New Zealand

|

Greater China

|

India

|

Japan

|

Korea

|

Taiwan

|

2011 YTD returns

|

-2.88%

|

-4.94%

|

-2.63%

|

-4.97%

|

-12.75%

|

-0.30%

|

-2.09%

|

-4.08%

|

12 month returns

|

5.56%

|

4.79%

|

11.96%

|

6.03%

|

-6.76%

|

6.73%

|

6.56%

|

4.47%

|

3 year annualised returns

|

6.53%

|

8.06%

|

8.79%

|

11.58%

|

3.20%

|

3.68%

|

4.17%

|

2.09%

|

Source: Eurekahedge

All strategies delivered positive returns over the last 12 months as well as in the long term. Event driven hedge funds gained 14.20% in 12 months on the back of a robust corporate activity environment which has provided significant opportunities for managers. Total M&A deals during the first nine months of 2011 reached a staggering US$419.2 billion within the Asia ex-Japan region, an increase of 16 percent in comparison to the January to September 2010 period. CTA Asian hedge funds also delivered excellent performance, locking in a total return of 34.40% over three years, outperforming the average Asian hedge fund by 13.51% in absolute terms. Regional long/short equity managers delivered a three year total return of 19.81%, beating the global average long/short equity fund’s performance by 5.5 percentage points.

Figure 10: Performance of Asian hedge funds across strategic mandates

Table 5: Performance of Asian hedge funds across strategic mandates

|

Arbitrage

|

CTA/

managed futures

|

Distressed debt

|

Event driven

|

Fixed income

|

Long/

short equities

|

Macro

|

Multi-strategy

|

Relative value

|

2011 YTD returns

|

-0.66%

|

3.05%

|

1.65%

|

4.00%

|

3.60%

|

-3.87%

|

1.28%

|

-0.46%

|

-2.43%

|

12 month returns

|

3.67%

|

10.98%

|

10.29%

|

14.20%

|

8.34%

|

5.04%

|

3.00%

|

6.29%

|

2.00%

|

3 year annualised returns

|

4.20%

|

10.36%

|

4.88%

|

8.99%

|

6.07%

|

6.21%

|

7.31%

|

6.00%

|

8.87%

|

Source: Eurekahedge